Q1 GDP Might Miss the Real Q2 Signal

The Q1 GDP headline will get the attention. The more useful question is whether the quarter was truly weak, or just distorted by the noisiest parts of the report.

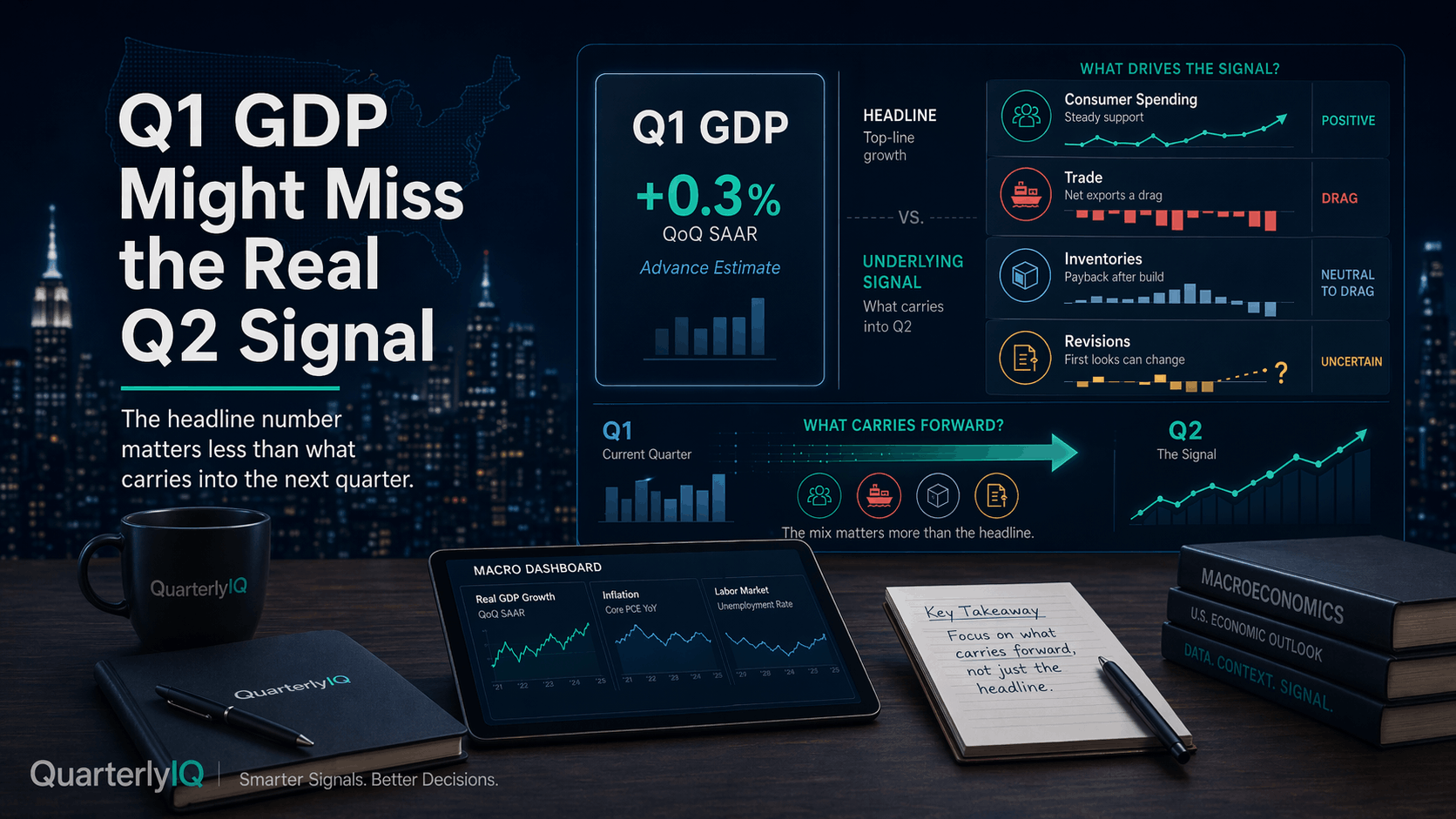

When the Q1 GDP report lands, the headline will do what GDP headlines usually do: grab attention and simplify a messy story. The advance estimate for Q1 2026 is scheduled for April 30, the same morning as the March personal income and outlays report.

That matters because GDP is often less settled than it first appears. In Q4 2025, BEA’s advance estimate showed real GDP growth of 1.4% annualized. The second estimate cut that to 0.7%. The third estimate cut it again to 0.5%. Same quarter, very different story.

So the better question is not just, “Was Q1 strong or weak?” It is, “What inside Q1 is likely to carry into Q2?”

Right now, the early signal looks mixed. The Atlanta Fed’s GDPNow model put Q1 growth at 1.3% as of April 9. That would be modest, but not necessarily alarming. A soft top-line GDP number can reflect real weakness, but it can also reflect noise from trade, inventories, or other parts of the report that do not always tell you much about the next quarter.

The consumer side of the economy still looks more resilient than fragile. In February, personal consumption expenditures rose 0.5% from the prior month, while personal income and disposable personal income each fell 0.1%. The personal saving rate fell to 4.0%. That is not a picture of a consumer pulling back hard. It looks more like households kept spending even as income growth softened.

Trade is one reason the headline could look weaker than the underlying handoff into Q2. In February, the U.S. goods and services deficit widened to $57.3 billion from $54.7 billion in January. Exports rose 4.2%, but imports rose 4.3%, and imports subtract from GDP. That means a quarter can look softer on paper even when demand is still decent. Sometimes the headline says “slowdown” when part of the story is simply that Americans and businesses bought more from abroad.

That is why the composition of GDP matters more than the first number. If Q1 comes in soft mainly because trade dragged on growth, that is a different setup than a quarter where household demand, business spending, and domestic activity all rolled over together. One is noisy. The other is more likely to leave a mark on Q2. The market should care about that difference.

What this means for sectors and stocks

The sector read-through depends on what is doing the damage.

If the GDP headline looks weak but consumer spending stays firm and the drag comes mostly from trade, then Q2 may still be decent for more cyclical areas such as industrials, transports, and consumer discretionary. If the report shows weaker demand under the surface, the market may lean more toward defensives like staples, utilities, and health care.

That is not a prediction. It is the framework. A weak headline alone does not tell you which sectors deserve caution. The internals do.

What to watch next

The first GDP print will matter, but the next few releases will matter more than usual. On April 30, investors get the Q1 GDP advance estimate and March personal income and outlays. On May 5, BEA releases the March trade report. On May 28, the second estimate for Q1 GDP arrives with corporate profits. That sequence should tell investors whether Q1 was the start of a real slowdown or just a noisy handoff into Q2.

Bottom line

Q1 GDP may tell you how the quarter ended.

It may not tell you what Q2 will feel like.

That is why the better move is to look past the headline and ask a simpler question: was the economy actually losing steam, or did the noisiest parts of GDP just make it look that way?

That is usually where the real signal is hiding.